The Fannie Mae HomeReady mortgage program provides an incredible opportunity to buy a home, or refinance an existing mortgage. This program offers flexible requirement guidelines, competitive loan terms, and a low down payment option.

Fannie Mae HomeReady Mortgage Program Highlights

This unique program offers many advantages. You can view some of the highlights of HomeReady below:

- 3% down payment – You can finance up to 97% of your home purchase (97% LTV). You can also borrower the money used for your down payment, it does not have to come from your own funds.

- Affordable and cancellable mortgage insurance – The mortgage insurance on HomeReady is cheaper than other types of mortgages, including other conventional loans. You also may cancel your mortgage insurance once you have at least 20% equity (an 80% LTV or lower).

- Lower interest rates – The interest rates on HomeReady are lower than other types of mortgage loans, including conventional and government-insurance mortgages, such as FHA loans.

- Flexible income requirements – There is a great deal of flexibility in what income can be used to qualify for your mortgage. As mentioned above, you can use the income from all members in your household, whether they are on the loan or not. You can also use “boarder income”, which is income collected from renting out a room or portion of your house, such as a basement, or “mother-in-law” unit, which are also known as accessory dwelling units (ADU). Also, you can have a non-occupant co-borrower, which in other words, means you can have a cosigner that does not live at the residence you purchase.

Would you like to find out if you qualify for the HomeReady mortgage program? We can help match you with a mortgage lender that offers HomeReady loans in your location.

Click here to have a HomeReady lender contact you

Fannie Mae HomeReady Mortgage Program Requirements

Below are some of the requirements you must satisfy in order to be eligible for the HomeReady program:

- Credit score – The minimum credit score requirement is 620. Some lenders may require a higher score, but that seems to be the lowest FICO score that is being accepted.

- Not a current homeowner – You must not currently own any other property. You do NOT have to be a first time home buyer, but you can not currently be a homeowner.

- Homeowner class – You must complete a homeowner education course. This is known as the Framework homebuyer education course. Only one borrower needs to participate, and it can be done online, and at your own pace.

- Down Payment – The minimum down payment requirement is 3%. This money can be borrowed, gifted, or even come from a down payment assistance program. You do not have to use your own funds (“cash on hand” or from a bank account that you own), as is often required with other types of mortgages.

- Income Requirements – As mentioned above, there is a lot of flexibility in what income can be used to qualify. The maximum DTI ratio (debt-to-income ratio) is 50%. Fortunately, you can use the income from all members in your household to qualify, whether they are related or not. Also, they do not have to be on the loan, so anyone living in the house can use their income to help you qualify.

- Income Limits – There are also income limits restricting the amount of money you can make. There are not any income limits in many regions, such as areas with lower income, high minority areas, and designated disaster areas. In more affluent cities, the income limits are 100% of the average median income of that location. You can look up the income limits by searching an address on the Fannie Mae website.

These are some of the basic requirements for the HomeReady mortgage program. If you would like to find out if you qualify for HomeReady, we can help match you with a lender in your location. To have a lender contact you, fill out this form. You may also view some HomeReady lenders below.

List of HomeReady Mortgage Lenders

Below is a list of some of the best mortgage lenders that offer the HomeReady program. However, we will help you to identify the best option for your location by completing this short Homeready Form.

1.) Prosperity Home Mortgage – Contact

2.) Dream Home Financing – Contact

3.) NewRez Wholesale – Contact

4.) Nola Lending Group – Contact

5.) American Internet Mortgage – Contact

6.) Omega Mortgage Group – Contact

7.) American Financing – Contact

8.) PennyMac Loan Services – Contact

9.) Movement Mortgage – Contact

10.) Better Mortgage – Contact

The lenders featured above all good options for the HomeReady program. If you would like some assistance finding a HomeReady lender, we can help match you with a lender in your location.

Click here to get matched with a mortgage lender

Fannie Mae HomeReady Income Limits

The HomeReady program has income limits which will prevent high earning individuals from utilizing the program while helping those who may be struggling to afford a home in their geography.

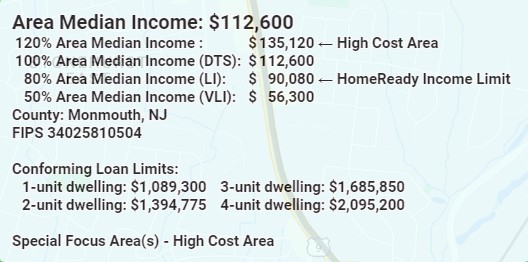

The HomeReady income limits applicants to those who make no more than 80% of the area’s median income (AMI). If you use this HomeReady median area income looking tool, you can input your zip code or address and find what the median income is. If you make the median amount or less, then you may qualify for the HomeReady program.

Here is a chart of the Homeready income looking tool. In this one example, you can see the median income is clearly referenced. Now, use the link to input your area to see what the median income is for you.

HomeReady DTI Limits

The maximum allowable DTI ratio by DU (Desktop Underwriter) for the HomeReady program is up to 50%. This DTI ratio is higher than what conventional loans will allow for which helps lower income families to afford a home.

The program will allow non occupying cosigners to help meet the DTI limits for the HomeReady program. Additional applicants will also need to meet the minimum credit score requirements.

HomeReady Home Ownership Education

One of the requirements of the HomeReady mortgage approval is to go through a HomeReady home ownership education program. In this program, you will learn the following:

- Understanding how to be a responsible homeowner

- Education on the HomeReady mortgage process and the requirements

- Review on appraisals, inspections, insurance requirements, and more

There are multiple ways to find a course from the Fannie Mae website linked earlier. Your mortgage application cannot be approved without confirmation that this program has been completed.

HomeReady Multi Family Guidelines

If you are interested in purchasing a multi family home using the HomeReady program, please note the maximum loan to value ratio is 85%. This means you are restricted to the benefits of the higher LTV requirement and having the ability to remove PMI at some point in the future.

Those who wish to purchase a multi family home but have a small down payment should consider using an FHA loan instead. The down payment is only 3.5% and the debt to income ratio allowed is higher.

HomeReady Refinance

You can refinance with the HomeReady program to lower your interest rate or improve your term. If you are looking to cash out equity, you may want to consider a different loan program. With HomeReady, only limited cash outs are permitted and usually to only include closing costs.

Another refinance option if your plan was to use the funds to update the home is the FHA 203k rehab loan. With this program, you can borrow more than what the home is worth to pay for the rehabilitation.

HomeReady Mortgage Rates

The HomeReady mortgage rates are extremely competitive especially if you have good credit. You can expect the rates to be as good if not better than a conventional or FHA loan.

If you need a rate quote for a HomeReady mortgage then we can help you. Just complete this short request quote form.

FHA vs HomeReady Mortgages

The decision to go with an FHA or a HomeReady loan will vary depending upon each borrower’s situation. It will be important to fully understand both programs before making a final decision.

This FHA vs HomeReady comparison chart will provide you with some of the basic differences

| Program Feature | HomeReady | FHA |

| Minimum Credit Score | 620 | 500 |

| Minimum Down Payment | 3% | 3.5% |

| Income Limits | Yes | No |

| Maximum DTI | 50% | 56.9% |

| PMI Can Be Cancelled | Yes | No |

| Cash Out Refinance Option | No | Yes |

| Rehab Option | No | Yes |

| Non Traditional Income | Yes | No |

How to Apply for a HomeReady Mortgage

Applying for a HomeReady mortgage is easier today than in the past. Applications can be done online and your loan officer can issue a pre-approval the same day if the application is complete.

The first step is to complete this form so a loan officer can contact you to begin the process.

Once you speak with a loan officer, your assistance in completing the application quickly and providing all of the necessary documents will be critical in securing your pre approval.

Frequently Asked Questions

What is the Minimum FICO Score for HomeReady mortgages?

Can you use HomeReady to purchase an investment property?

No, you may not purchase an investment property, vacation home, or second home using this program. It is only available to purchase a primary residence that you will occupy.

Is HomeReady the same as the Fannie Mae Conventional 97 Loan?

No, these are two separate Fannie Mae programs. Both only require a 3% down payment, so they are often confused as being the same. HomeReady is geared for low-to-moderate income households, whereas the conventional 97 loan is geared for borrowers with good credit and income.

How does the HomeReady compare to FHA loans?

There are some clear advantages of the HomeReady program compared to FHA loans. This includes easier qualification guidelines, lower interest rates, and the option to cancel your mortgage insurance once the LTV is below 80%. FHA loans require that you pay mortgage insurance no matter what the LTV is, making them more costly over time. We recommend that you first see if you qualify for HomeReady, and if are not approved, then apply for an FHA loan.

How does HomeReady compare to the Freddie Mac Home Possible program?

HomeReady and Home Possible are both very similar, providing a low down payment mortgage that is easy to qualify for. Determining which is better will depend on your unique situation. One advantage of the Freddie Mac Home Possible program has over the HomeReady program is that if you buy a 2-4 unit property with HomeReady, you will have to source the funds for your down payment (meaning it can not be borrowed or gifted).

Can you refinance a property with HomeReady?

Yes, you may use the HomeReady program to refinance an existing mortgage. This includes a limited cash out refinance option with a 97% max LTV ratio.

What types of properties are eligible?

The HomeReady program is available for almost any type of residential property, including single family residences, a multi-unit property (2-4 units), condominiums, co-ops, and manufactured homes.

Are seller concessions allowed?

Yes, seller concessions are allowed. The seller can pay your closing costs, and even provide the funds to use for your down payment.

Do my co-habitants living in my home have to be legal residents?

No, your co-habitants (people living in your home) do not have to be legal residents. They can be undocumented immigrants, and you can still use their income to help you qualify.

Is this program offered by all mortgage lenders?

Any mortgage lender that is Fannie Mae approved is usually eligible to issue this type of loan. If you would like some helping finding a lender that offers the HomeReady program, we can help match you with one in your location. If you would like to have a HomeReady lender contact you, fill out this form.

What Others Say About the HomeReady Program

Mortgage Insider – “The HomeReady program is great for people who have good credit and need a low down payment mortgage option.”

Eric Jeanette – “Home buyers who have non traditional income and credit scores over 620 may benefit by applying for a HomeReady mortgage.”