FHA Approved Lenders in Maryland

FHA loans are a good option for a variety of borrowers. This includes those who want to place a low down payment, as well as those that struggle with some credit issues. Some think of FHA loans as subprime mortgages, but they technically are not. However, they do serve borrowers that can not qualify for a prime mortgage or conventional loan.

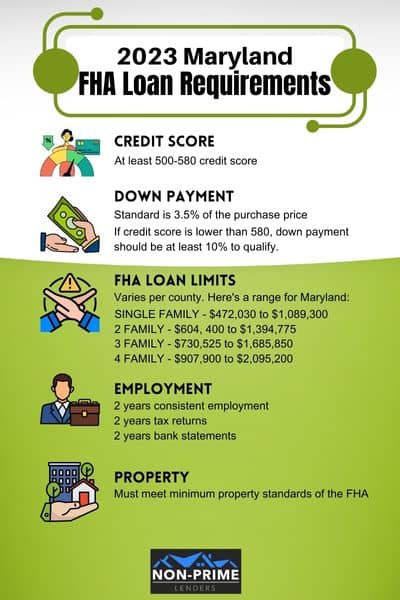

2024 Maryland FHA Loan Requirements

You may view the primary FHA loan requirements for Maryland below. Each individual FHA approved lender may have some of their own loan requirements in addition to these.

Credit – Most Maryland FHA lenders will require that you have at least a 580 credit score. However, we work with a few lenders that will go down to a 500 credit score.

Down Payment – The standard down payment requirements for a FHA loan is 3.5% of the purchase price. So on a $200,000 loan, the down payment would need to be $7,000. If your credit score is below a 580, you may need to place as much as 10% down in order to qualify.

FHA Loan Limits – The FHA loan limits are the maximum loan amount available in a particular county. You can view the 2024 FHA loan limits for Maryland, on this page.

Employment – FHA loans require that you prove 2 years of consistent employment. You will need to provide at 2 years tax returns, and most lenders want to see your 2 most recent bank statements as well.

Property – The FHA has property requirements, which includes what are known as “minimum property standards”. The home you want to purchase must undergo an appraisal and meet these guidelines, which relate to the condition of the home. The appraisal must also verify the value of the property.

Mortgage Insurance – There are two types of mortgage insurance premiums (MIP) required for all FHA loans. The first type is upfront mortgage insurance premiums (UPMIP), which is 1.75% of the total loan amount. This fee can be included in the loan, and does not need to be paid out of pocket. The second type of mortgage insurance premiums is paid monthly, which is 0.85% of the loan amount (calculated annually, but paid monthly as part of the monthly mortgage payment).

These are the standard requirements for a FHA loan. When you apply, if you are approved, you will be provided a checklist of requirements known as “loan conditions”, which will outline what you must provide in order for the loan to close.

Click here to find out if you qualify for a FHA loan

George Makouts from Novus Home Mortgage in Maryland: “The FHA’s backing of loans often allows approved lenders to offer more lenient qualification criteria, enabling a broader spectrum of individuals, including those with a modest income, to step onto the property ladder.”

Best FHA Lenders in Maryland

Below are our top picks for the best FHA lenders in Maryland. However, your scenario may be better suited for a different lender. Contact us here to get a personalized quote.

1.) Quicken Loans

2.) Guaranteed Rate

4.) Freedom Mortgage

5.) Loan Depot

6.) U.S. Bank

7.) Secured Funding Corporation

Please note: We are not affiliated with all mortgage lenders that are featured on our website. We include who we consider to be the best lenders for various mortgage programs. If you would like some help getting connected with a FHA lender in Maryland, please fill out this form.

Maryland FHA Cash Out Refinance

You may qualify for a cash out refinance of your home in Maryland using FHA financing. The maximum FHA loan amount when cashing out equity is 80% of the appraised value.

With the FHA cash out refinance, you will need to provide all of the traditional income and asset documentation and the home will need to be appraised. When the real estate market is high, you have a unique opportunity to access the equity before the values decline. If you are thinking about this as an option, we can help you with a quote.

FHA Loan in Maryland with a Bankruptcy

If you have a bankruptcy in your history, we still can help you to get an FHA loan. If your bankruptcy was a chapter 7 and it was discharged less than two years ago, you will need a hardship exception to secure an approval. The exceptions are not granted too often so your scenario will need to be related to a dire situation.

If your bankruptcy was a chapter 13, we can help you to get an FHA loan after you have made just 12 bankruptcy payments. There is no need to wait until the discharge date.

Read more about getting a mortgage after a bankruptcy.

Frequently Asked Questions

Are FHA loans only for first time home buyers?

No, FHA loans are not restricted to first time home buyers. If you have owned a home before, you may still get a FHA loan. However, you may only have one FHA loan, and they are only available for primary residences.

How do I apply for a FHA loan in Maryland?

It is very easy to get pre-qualified or to apply for a FHA loan. We recommend having us match you with a FHA lender in Maryland based on your personal needs (such as estimated credit and loan amount). To be matched with a FHA lender, please fill out this form.

Is down payment assistance available for FHA loans?

Yes, if you qualify for down payment assistance, you can be used with a FHA loan. There are many programs available that provide funds to use for down payment assistance. We can help you find out if you qualify for any of them.

What are the options to refinance a FHA loan?

The FHA offers two different programs for refinancing a FHA loan. This includes the FHA streamline refinance, which allows you to easily lower your interest rate and mortgage payment (and does not require a credit check, income documentation, or a new appraisal). The other option for refinancing an existing FHA loan, is the FHA cash out refinance, which allows you to pull out money from the equity in your home.

Are cosigners allowed on FHA loans?

Yes, cosigners are allowed on FHA loans. At least one of the borrowers must occupy the property. Non-occupying co-borrowers are allowed though, which means the person cosigning does not need to live at the property that is financed using a FHA loan.

How long after a bankruptcy can you get a FHA loan?

The FHA rules state that you must wait at least 2 years after filing a chapter 7 bankruptcy. For a chapter 13, you only need to wait until you have successfully made 12 months of payments. Additionally, you will need to provide the court trustee’s written approval. Also, keep in mind that the clock doesn’t start upon filing, but rather once the bankruptcy has been discharged.

How long after a foreclosure can you get a FHA loan?

The FHA rules state that you must wait at least 3 years before you are eligible for a FHA loan. However, there is an exception to this rule if there were “extenuating circumstances”, such as a job loss. You would also have to show some improvements to your credit since the foreclosure. In the event that the circumstances and credit improvements are satisfactory, you would only have to wait until after 1 year before you can apply for a FHA loan.